Whether you’ve just retired or you’re thinking about retirement, you may be considering your options and trying to picture a whole new stage of your life. And you’re not alone. Research from the Retirement Industry Trust Association (RITA) shows 10,000 Baby Boomers reach the typical retirement age (65) every day, and only 47% of the people in that generation have already retired.

If this sounds like you, one thing worth considering is whether or not your current home will suit your new lifestyle. If your home doesn’t have the features or benefits you’re looking for, the good news is, you may be in a better position to move than you realize.

That’s because, if you already own a home, you’ve likely built-up significant equity, and that can help you fuel your next move. According to the National Association of Realtors (NAR):

“A homeowner who purchased a typical home five years ago would have gained $125,300 from just price appreciation alone.”

In fact, over the last twelve months, CoreLogic reports the average homeowner in the United States gained roughly $64,000 in equity due to home price appreciation.

You can use your equity to help you achieve your homeownership goals. Whether you want to downsize, move closer to loved ones, or buy a home in a dream destination, your equity can help get you there. It may be some (if not all) of what you’d need as your down payment on a home that better fits your changing needs.

To find out how much equity to have in your home, reach out to a trusted real estate professional today.

Bottom Line

Retirement is a big step and so is buying or selling a home. As you move into this new phase of life, let’s connect so you have an expert to guide you through the process as you sell your current home and give you expert advice as you buy one that’ll better suit your needs.

If you’re thinking of buying or selling a house, you’re at an exciting decision point. And anytime you make a big decision like that, one thing you should always consider is timing. So, what does the rest of the year hold for the housing market? Here’s what experts have to say.

The Number of Homes Available for Sale Is Likely To Grow

There are early signs housing inventory is starting to grow and experts say that should continue in the months ahead. According to Danielle Hale, Chief Economist at realtor.com:

“The gap between this year’s homes for sale and last year’s is one-fifth the size that it was at the beginning of the year. The catch up is likely to continue, . . . This growth will mean more options for shoppers than they’ve had in a while, even though inventory continues to lag pre-pandemic normal.”

As a buyer, having more options is welcome news. Just remember, housing supply is still low, so be ready to act fast and put in your best offer up front.

As a seller, your house may soon face more competition when other sellers list their homes. But the good news is, if you’re also buying your next home, having more options to choose from should make that move-up process easier.

Mortgage Rates Will Likely Continue To Respond to Inflationary Pressures

Experts also agree inflation should continue to drive up mortgage rates, albeit more moderately. Odeta Kushi, Deputy Chief Economist at First American, says:

“… ongoing inflationary pressure remains likely to push mortgage rates even higher in the months to come.”

As a buyer, work with trusted real estate professionals, including your lender, so you can learn how rising mortgage rate environments impact your purchasing power. It may make sense to buy now before it costs more to do so, if you’re ready.

As a seller, rising mortgage rates are motivating some homeowners to make a move up sooner rather than later. If you’re planning to buy your next home, talk to a trusted real estate advisor to decide how to time your move.

Home Prices Are Projected To Continue To Climb

Home prices are forecast to keep appreciating because there are still fewer homes for sale than there are buyers in the market. That said, experts agree the pace of that appreciation should moderate – but home prices won’t fall. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“Prices throughout the country have surged for the better part of two years, including in the first quarter of 2022. . . Given the extremely low inventory, we’re unlikely to see price declines, but appreciation should slow in the coming months.”

As a buyer, continued home price appreciation means it’ll cost you more to buy the longer you wait. But it also gives you peace of mind that, once you do buy a home, it will likely grow in value. That makes it historically a good investment and a strong hedge against inflation.

As a seller, price appreciation is great news for the value of your home. Again, lean on a professional to strike the right balance of the best conditions possible for both selling your house and buying your next one.

Bottom Line

Whether you’re a homebuyer or seller, you need to know what’s happening in the housing market, so you can make the most informed decision possible. Let’s connect to discuss your goals and what lies ahead, so you can pick your best time to make a move.

How Homeownership Can Help Shield You from Inflation

If you’re following along with the news today, you’ve likely heard about rising inflation. You’re also likely feeling the impact in your day-to-day life as prices go up for gas, groceries, and so much more. These rising consumer costs can put a pinch on your wallet and make you re-evaluate any big purchases you have planned to ensure they’re still worthwhile.

If you’ve been thinking about purchasing a home this year, you’re probably wondering if you should continue down that path or if it makes more sense to wait. While the answer depends on your situation, here’s how homeownership can help you combat the rising costs that come with inflation.

Homeownership Offers Stability and Security

Investopediaexplains that during a period of high inflation, prices rise across the board. That’s true for things like food, entertainment, and other goods and services, even housing. Both rental prices and home prices are on the rise. So, as a buyer, how can you protect yourself from increasing costs? The answer lies in homeownership.

Buying a home allows you to stabilize what’s typically your biggest monthly expense: your housing cost. If you get a fixed-rate mortgage on your home, you lock in your monthly payment for the duration of your loan, often 15 to 30 years. James Royal, Senior Wealth Management Reporter at Bankrate, says:

“A fixed-rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same.”

So even if other prices rise, your housing payment will be a reliable amount that can help keep your budget in check. If you rent, you don’t have that same benefit, and you won’t be protected from rising housing costs.

Use Home Price Appreciation to Your Benefit

While it’s true rising mortgage rates and home prices mean buying a house today costs more than it did a year ago, you still have an opportunity to set yourself up for a long-term win. Buying now lets you lock in at today’s rates and prices before both climb higher.

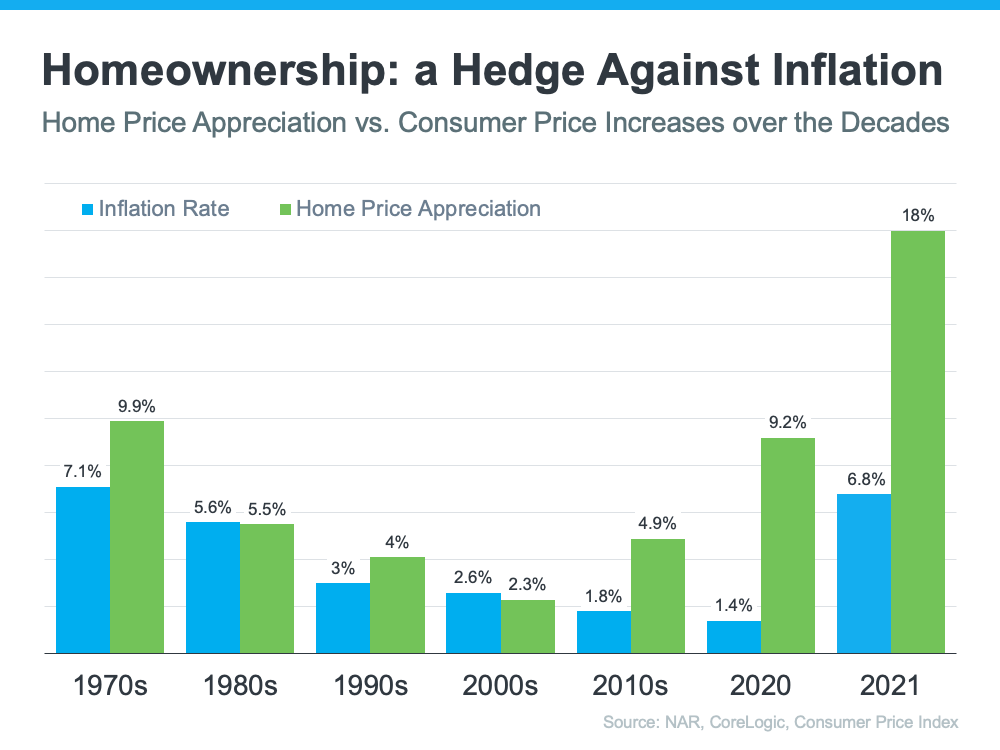

In inflationary times, it’s especially important to invest your money in an asset that traditionally holds or grows in value. The graph below shows how home price appreciation outperformed inflation in most decades going all the way back to the seventies – making homeownership a historically strong hedge against inflation (see graph below):

So, what does that mean for you? Today, experts say home prices will only go up from here thanks to the ongoing imbalance in supply and demand. Once you buy a house, any home price appreciation that does occur will be good for your equity and your net worth. And since homes are typically assets that grow in value (even in inflationary times), you have peace of mind that history shows your investment is a strong one.

Bottom Line

If you’re ready to buy a home, it may make sense to move forward with your plans despite rising inflation. If you want expert advice on your specific situation and how to time your purchase, let’s connect.

On the Fence of Whether or Not To Move This Spring? Consider This.

If you’re thinking of selling your house, it may be because you’ve heard prices are rising, listings are going fast, and sellers are getting multiple offers on their homes. But why are conditions so good for sellers today? And what can you expect when you move? To help answer both of those questions, let’s turn to the data.

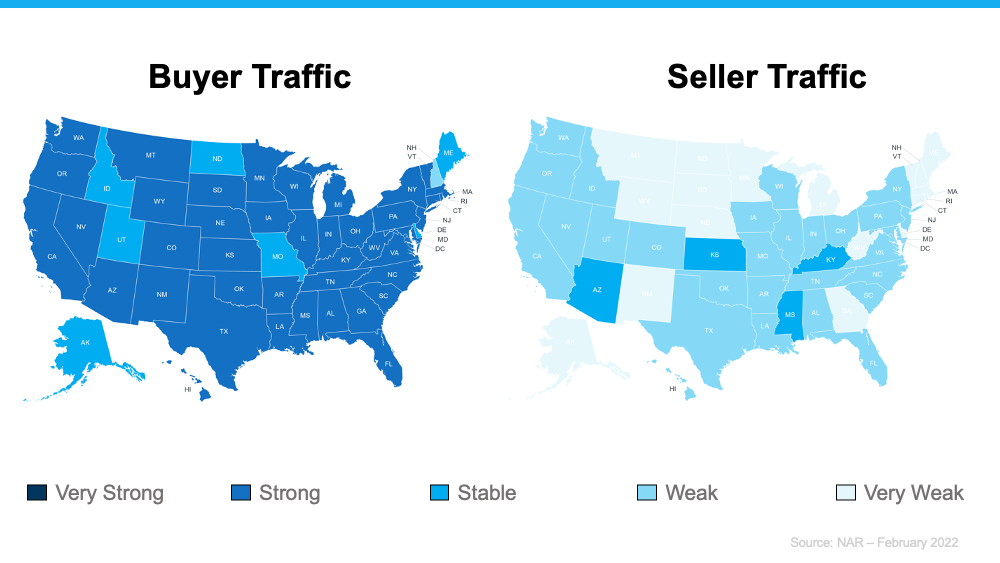

Today, there are far more buyers looking for homes than sellers listing their houses. Here are the maps of the latest buyer and seller traffic from the National Association of Realtors (NAR) to help paint the picture of what this looks like:

Notice how much darker the blues are on the left. This shows buyer traffic is strong today. In contrast, the much lighter blues on the right indicate weak or very weak seller traffic. In a nutshell, the demand for homes is significantly greater than what’s available to purchase.

What That Means for You

You have an incredible advantage when you sell your house under these conditions. Since buyer demand is so high at a time when seller traffic is so low, there’s a good chance buyers will be competing for your house.

According to NAR, in February, the average home sold got 4.8 offers. When buyers have to compete with one another like this, they’ll do everything they can to make their offer stand out. This could play to your favor and mean you’ll see things like waived contingencies, offers over asking price, earnest money deposits, and more. Selling when demand is high and supply is low sets you up for a big win.

If you’re also looking to buy a house, you may be tempted to focus more on just the seller traffic map and wonder if it means you’ll have trouble finding your next home. But remember this: perspective is key. As Danielle Hale, Chief Economist at realtor.com, says:

“The limited number of homes for sale is a lesson in perspective. This same stat that frustrates would-be homebuyers also means that today’s home sellers enjoy more limited competition than last year’s home sellers.”

If you look at the big picture, the opportunity you have as a seller today is unprecedented. Last year was a hot sellers’ market. This year, inventory is even lower, and that means an even bigger opportunity for you. Even though finding your next home in a market with low inventory can be challenging, is that concern worth passing on some of the best conditions sellers have ever seen?

As added peace of mind, remember real estate professionals have been juggling this imbalance of supply and demand for nearly two years, and they know how to help both buyers and sellers find success when they move. A skilled agent can help you capitalize on the great opportunity you have as a seller today and guide you through the buying process until you find the perfect place to call your next home.

Bottom Line

If you’re ready to move, you have an incredible opportunity in front of you today. That said, if the timing isn’t right, don’t feel pressure to make a move. This market won’t last forever, true, but with any investment–no matter how good or bad–the timing needs to be right for YOU!

Why This Housing Market Is Not a Bubble Ready To Pop

Homeownership has become a major element in achieving the American Dream. A recent report from the National Association of Realtors (NAR) finds that over 86% of buyers agree homeownership is STILL the American Dream.

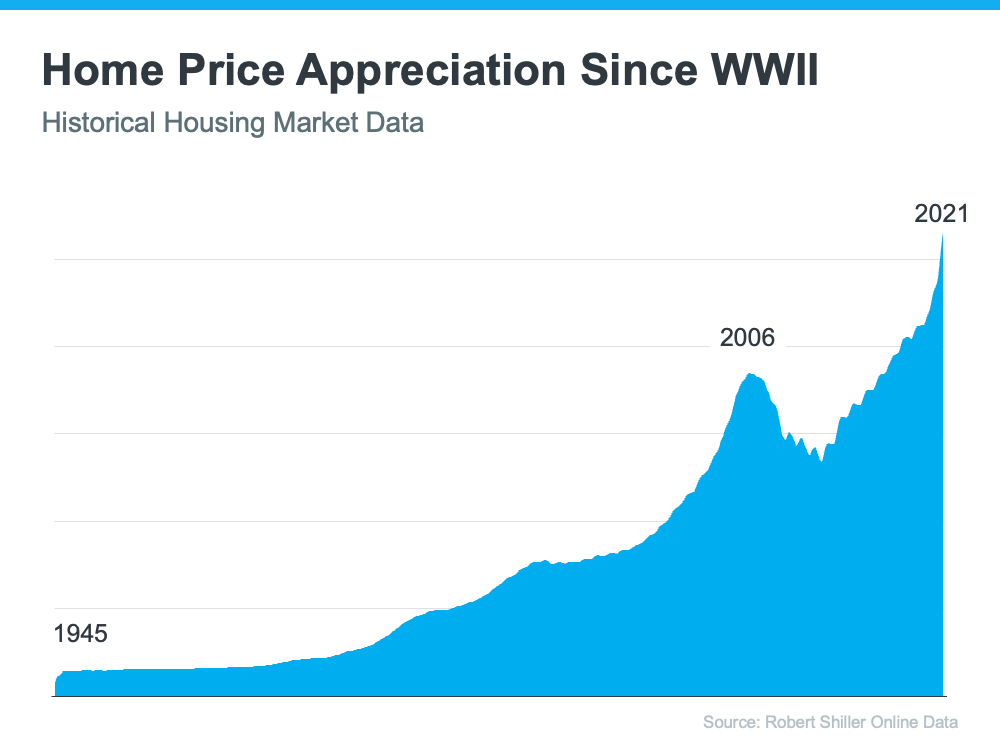

Prior to the 1950s, less than half of the country owned their own home. However, after World War II, many returning veterans used the benefits afforded by the GI Bill to purchase a home. Since then, the percentage of homeowners throughout the country has increased to the current rate of 65.5%. That strong desire for homeownership has kept home values appreciating ever since. The graph below tracks home price appreciation since the end of World War II:

The graph shows the only time home values dropped significantly was during the housing boom and bust of 2006-2008. If you look at how prices spiked prior to 2006, it looks a bit like the current spike in prices over the past two years. That may lead some people to be concerned we’re about to see a similar fall in home values as we did when the bubble burst. To help alleviate those worries, let’s look at what happened last time and what’s happening today.

What Caused the Housing Crash 15 Years Ago?

Back in 2006, foreclosures flooded the market. That drove down home values dramatically. The two main reasons for the flood of foreclosures were:

1. Many purchasers were not truly qualified for the mortgage they obtained, which led to more homes turning into foreclosures.

2. A number of homeowners cashed in the equity on their homes. When prices dropped, they found themselves in an underwater situation (where the home was worth less than the mortgage on the house). Many of these homeowners walked away from their homes, leading to more foreclosures. This lowered neighboring home values even more.

This cycle continued for years.

Why Today’s Real Estate Market Is Different

Here are two reasons today’s market is nothing like the one we experienced 15 years ago.

1. Today, Demand for Homeownership Is Real (Not Artificially Generated)

Running up to 2006, banks were creating artificial demand by lowering lending standards and making it easy for just about anyone to qualify for a home loan or refinance their current home. Today, purchasers and those refinancing a home face much higher standards from mortgage companies. That is not the case today.

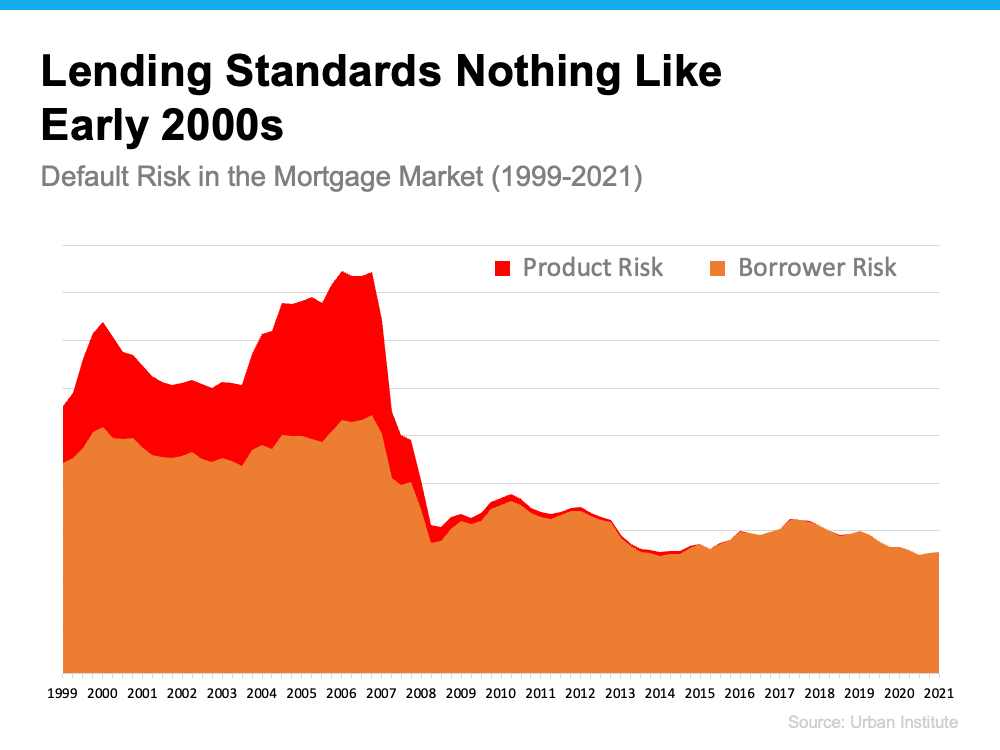

Data from the Urban Institute shows the amount of risk banks were willing to take on then as compared to now.

There’s always risk when a bank loans money. However, leading up to the housing crash 15 years ago, lending institutions took on much greater risks in both the person and the mortgage product offered. That led to mass defaults, foreclosures, and falling prices.

Today, the demand for homeownership is real. It’s generated by a re-evaluation of the importance of home due to a worldwide pandemic. Additionally, lending standards are much stricter in the current lending environment. Purchasers can afford the mortgage they’re taking on, so there’s little concern about possible defaults.

And if you’re worried about the number of people still in forbearance, you should know there’s no risk of that causing an upheaval in the housing market today based upon current lending standards.

2. People Are Not Using Their Homes as ATMs Like They Did in the Early 2000s

As mentioned above, when prices were rapidly escalating in the early 2000s, many thought it would never end. They started to borrow against the equity in their homes to finance new cars, boats, and vacations. When prices started to fall, many of these homeowners were underwater, leading some to abandon their homes. This increased the number of foreclosures and the cycle continued.

Homeowners didn’t forget the lessons of the crash as prices skyrocketed over the last few years. Black Knight reports that tappable equity (the amount of equity available for homeowners to access before hitting a maximum 80% loan-to-value ratio, or LTV) has more than doubled compared to 2006 ($4.6 trillion to $9.9 trillion).

The latest Homeowner Equity Insights report from CoreLogic reveals that the average homeowner gained $55,300 in home equity over the past year alone. Odeta Kushi, Deputy Chief Economist at First American, reports:

“Homeowners in Q4 2021 had an average of $307,000 in equity – a historic high.”

ATTOM Data Services also reveals that 41.9% of all mortgaged homes have at least 50% equity. These homeowners will not face an underwater situation even if prices dip slightly. Today, homeowners are much more cautious.

Bottom Line

The major reason for the housing crash 15 years ago was a tsunami of foreclosures. With much stricter mortgage standards and a historic level of homeowner equity, the fear of massive foreclosures impacting today’s market is not realistic.

Being intentional and competitive are musts when buying a home this season. That’s why pre-approval is so important today. Pre-approval from a lender is the only way to know your true price range and how much money you can borrow for your loan. Peter Warden, Editor of The Mortgage Reports, explains:

“The lender will check out your personal finances and issue you a letter confirming the amount you’re eligible to borrow. This not only gives you a firm budget for house hunting, but also lets sellers know you’re qualified to make an offer.”

Why does that matter so much today? There are many more buyers looking for homes today than there are homes available for sale, and that’s creating some serious competition. According to the National Association of Realtors (NAR), the average home is getting 4.8 offers per sale. As a result, bidding wars are still common.

Your pre-approval gives you a leg up in these situations. That’s because you know exactly what you’re approved to borrow before you write your offer, and it lets the seller know you’re qualified to buy their home. This helps both you and the seller feel confident in what you’re bringing to the table. And that puts you in a better position to potentially win a bidding war.

As Warden puts it:

“There’s another important reason to get preapproved, too. And that’s because there are way more buyers than homes in today’s market — which means you need to be ultra-prepared if you want to win a bidding war. Most sellers are getting multiple offers right now. And most won’t even entertain an offer without a preapproval letter included.”

Every advantage you can gain as a buyer is crucial in a market that’s constantly changing. Mortgage rates are rising, home prices are going up, and lending institutions are regularly updating their standards. You’re going to need guidance to navigate these waters, so it’s important to have a team of professionals, such as a loan officer and a trusted real estate advisor, on your side. They’ll help make sure you’re ready to put your best foot forward.

Bottom Line

Getting pre-approved for a mortgage helps you better understand what you can afford and signals to sellers you’re serious about purchasing their home. Let’s connect so you have the tools you need to succeed as a homebuyer in today’s market

For many young or first-time homebuyers, purchasing a home can feel intimidating. A recent survey shows some homebuyers ages 25 to 40 may be unsure about the homebuying process and what they can afford. It found:

“1 in 4 underestimated their buying potential by $150k or more”

“1 in 4 underestimated the increase in value by $100k or more”

“47% don’t know what a good interest rate is”

Because they feel uncertain, many young homebuyers have given up on their search, or worse, they’ve decided homebuying isn’t for them and never started on their journey to begin with.

If you’re interested in buying but aren’t sure where to begin, here are three key concepts about homeownership you should understand before you get started.

1. What You Need To Know About Down Payments

Saving for a down payment is sometimes viewed as one of the biggest obstacles for homebuyers, but that doesn’t have to be the case. As Freddie Macsays:

“The most damaging down payment myth—since it stops the homebuying process before it can start—is the belief that 20% is necessary.”

According to the most recent Home Buyers and Sellers Generational Trends Report from the National Association of Realtors (NAR), the median down payment for homes purchased between July 2019 and June 2020 was only 12%. That number is even lower when we control for age – for buyersin the 22 to 30 age range, the median down payment was only 6%.

2. You May Be Able To Afford More Home Than You Think

Working remotely, exercising, and generally spending more time than ever in our homes has changed what many people are looking for in their living space. However, some young homebuyers don’t feel they can afford a home that suits their growing needs and have decided to continue renting instead. That means they’ll miss out on some of the long-term benefits of owning a home. As an article recently published by NAR points out:

“Many young adults are underestimating how much they need for homeownership, the survey finds. Millennials underestimated how much home they can afford right now, how much interest they would pay over a 30-year mortgage, and how much home values appreciate, on average, over 10 years…”

Knowing how much home you can afford when starting the buying process is critical and could be the game-changer that gets you from renting to buying.

3. Homeownership Will Become Less Affordable the Longer You Wait

Finally, with mortgage rates starting to rise along with home prices appreciating, putting off buying a home now could cost you much more later. Sam Khater, Chief Economist at Freddie Mac,notes:

“As the economy progresses and inflation remains elevated, we expect that rates will continually rise in the second half of the year.”

Most experts forecast interest rates will rise in the months ahead, and even the smallest increase can influence your buying power. If you’ve been on the fence about buying a home, there’s no time like the present.

Bottom Line

If you feel overwhelmed by the prospect of starting your home search, you’re not alone. Let’s connect today so we can talk more about the process, what you’ll need to start your search, and what to expect.

What You Can Expect from the Spring Housing Market

As the spring housing market kicks off, you likely want to know what you can expect this season when it comes to buying or selling a house. While there are multiple factors causing some uncertainty, including the conflict overseas, rising inflation, and the first rate increase from the Federal Reserve in over three years — the housing market seems to be relatively immune.

Here’s a look at what experts say you can expect this spring.

1. Mortgage Rates Will Climb

Freddie Macreports the 30-year fixed mortgage rate has increased by more than a full point in the past six months. And despite some mild fluctuation in recent weeks, experts believe rates will continue to edge up over the next 90 days. As Freddie Macsays:

“The Federal Reserve raising short-term rates and signaling further increases means mortgage rates should continue to rise over the course of the year.”

If you’re a first-time buyer or a seller thinking of moving to a home that better fits your needs, realize that waiting will likely mean you’ll pay a higher mortgage rate on your purchase. And that higher rate drives up your monthly payment and can really add up over the life of your loan.

2. Housing Inventory Will Increase

There may be some relief coming for buyers searching for a home to purchase. Realtor.com recently reported that the number of newly listed homes has grown for each of the last two months. Also, the National Association of Realtors (NAR) just announced the months’ supply of inventory increased for the first time in eight months. The inventory of existing homes usually grows every spring, and it seems, based on recent activity, the next 90 days could bring more listings to the market.

If you’re a buyer who has been frustrated with the limited supply of homes available for sale, it looks like you could find some relief this spring. However, be prepared to act quickly if you find the right home.

If you’re a seller, listing now instead of waiting for this additional competition to hit the market makes sense. Your leverage in any negotiation during the sale will be impacted as additional homes come to market.

3. Home Prices Will Rise

Prices are always determined by supply and demand. Though the number of homes entering the market is increasing, buyer demand remains very strong. As realtor.com explains in their most recent Housing Report:

“During the final two weeks of the month, more new sellers entered the market than during the same time last year. . . . However, with 5.8 million new homes missing from the market and millions of millennials at first-time buying ages, housing supply faces a long road to catching up with demand.”

What does that mean for you? With the demand for housing still outpacing supply, home prices will continue to appreciate. Many experts believe the level of appreciation will decelerate from the high double-digit levels we’ve seen over the last two years. That means prices will continue to climb, just at a more moderate pace. Most experts are predicting home prices will not depreciate.

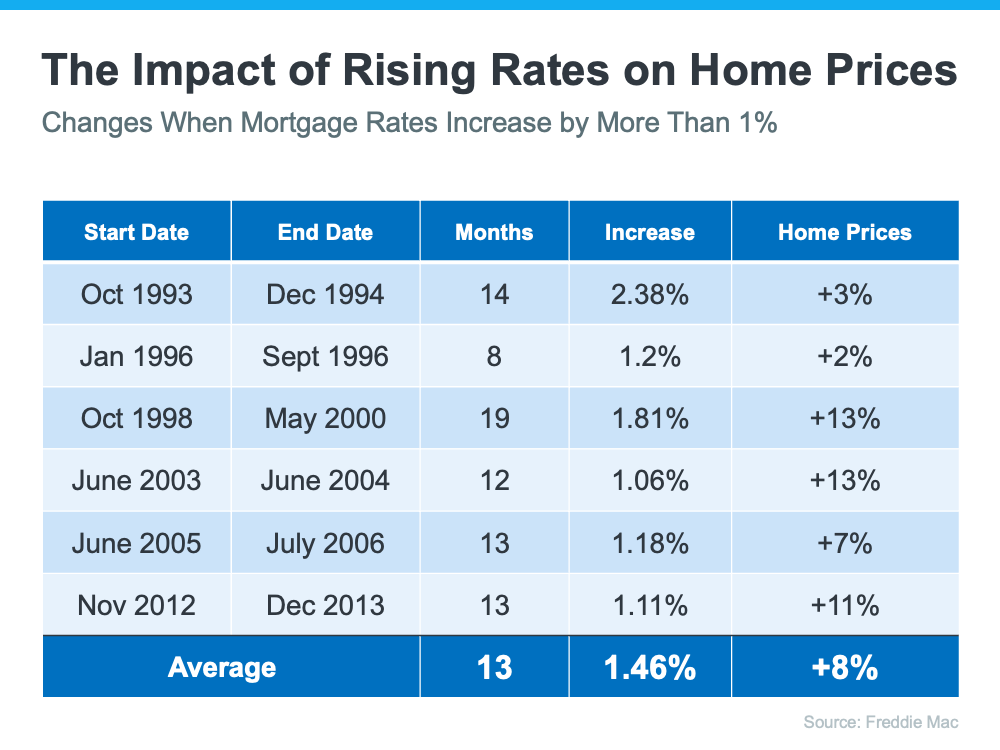

Won’t Increasing Mortgage Rates Cause Home Prices To Fall?

While some people may believe a 1% increase in mortgage rates will impact demand so dramatically that home prices will have to fall, experts say otherwise. Doug Duncan, Senior Vice President and Chief Economist at Fannie Mae, says:

“What I will caution against is making the inference that interest rates have a direct impact on house prices. That is not true.”

Freddie Mac studied the impact that mortgage rates increasing by at least 1% has had on home prices in the past. Here are the results of that study:

As the chart shows, mortgage rates jumped by at least 1% six times in the last thirty years. In each case, home values increased.

So again, if you’re a first-time buyer or a repeat buyer, waiting to buy likely means you’ll pay more for a home later in the year (as compared to its current value).

Bottom Line

There are three things that seem certain going into the spring housing market:

Mortgage rates will continue to rise

The selection of homes available for sale will modestly improve

Home prices will continue to appreciate, just at a slightly slower pace

If you’re thinking of buying, act now before mortgage rates and home prices increase further. If you’re thinking of selling, your best bet may be to sell soon so you can beat the increase in competition that’s about to come to market.

Remote Work Trends Mean Flexibility for First-Time Homebuyers

Today’s low inventory can be challenging for homebuyers, especially if you’re looking to purchase your first home. But if you’re one of many people who work remotely, you may have a great opportunity to use the flexibility you have at work to achieve your homebuying goals this year.

In a recent report, Arch Capital Services explains how the ongoing trend of remote work can open up more options for homebuyers:

“. . . This will enable those who are able to work from home on a part-time or hybrid basis to move slightly farther away from job centers. . . . For workers who secure full-time remote jobs, their place of residence will be determined by affordability and personal preferences.”

Basically, working from home is great news if you’re a first-time buyer trying to find a home that meets your needs and budget. Here’s a deeper look at how it could benefit you.

Extra Flexibility in Your Career Means Extra Flexibility in Your Home Search

If your job is 100% remote, you don’t have to be tied to a specific location or office. So, if you’ve been having a hard time finding what you want in your local area, it may be time to expand your search.

One option you could consider is moving to a place where you’ve always wanted to live, like the mountains, beach, or closer to loved ones. When you broaden your search radius to include those locations, it’ll give you additional homes to consider.

It could also allow you to search for a more affordable location where you have more options in your price range. This can help you achieve two goals – saving money and finding additional features that meet your needs. To truly highlight this benefit, a recent First Americanarticle discusses the great ways remote work can really help you with your homebuying goals. Ksenia Potapov, Economist at First American, says:

“For potential first-time home buyers, leveraging their house-buying power in more affordable markets can also help them buy more attractive homes – more square footage and rooms, more options for different home styles and neighborhood amenities – increasing the opportunity to find a home that suits their preferences.”

That means you can use your work flexibility to search for homes with the amenities you need at a lower price point.

Bottom Line

Remote work doesn’t just give you expanded flexibility for your career. If you’re no longer tied to a location because of your office, you have a great opportunity to expand your housing search. Let’s connect to explore how this can open up your options.

What’s Happening with Mortgage Rates, and Where Will They Go from Here?

Based on the Primary Mortgage Market Survey from Freddie Mac, the average 30-year fixed-rate mortgage has increased by 1.2% (3.22% to 4.42%) since January of this year. The rate jumped by more than a quarter of a point from just a week ago. Here’s a visual to show how mortgage rate movement throughout 2021 was steady compared to the rapid increase in mortgage rates this year:

Just a few months ago, Freddie Macprojected mortgage rates would average 3.6% in 2022. Earlier this month, Fannie Maeforecast mortgage rates would average 3.8% in 2022. As the chart above shows, rates have already surpassed those projections.

Sam Khater, Chief Economist at Freddie Mac, explained in a press release last week:

“This week, the 30-year fixed-rate mortgage increased by more than a quarter of a percent as mortgage rates across all loan types continued to move up. Rising inflation, escalating geopolitical uncertainty and the Federal Reserve’s actions are driving rates higher and weakening consumers’ purchasing power.”

Where Are Mortgage Rates Going from Here?

In a recent article by Bankrate, several industry experts weighed in on where rates might be headed going forward. Here are some of their forecasts:

Greg McBride, Chief Financial Analyst, Bankrate:

“With inflation figures continuing to surprise to the upside, mortgage rates will remain above 4.0% on the 30-year fixed.”

Nadia Evangelou, Senior Economist and Director of Forecasting, National Association of Realtors (NAR):

“While higher short-term interest rates will push up mortgage rates, I expect some of this impact to be mitigated eventually through lower inflation. Thus, I expect the 30-year fixed mortgage rate to continue to rise, although we aren’t likely to see the big jumps that occurred over the past few weeks.”

Len Kiefer, Deputy Chief Economist, Freddie Mac:

“Mortgage rates are likely to continue to move higher throughout the balance of 2022, although the pace of rate increases is likely to moderate.”

In a recent realtor.comarticle, another expert adds to the conversation:

Danielle Hale, Chief Economist, realtor.com:

“. . . As markets digest the Fed’s updated economic projections, I anticipate a continued increase in mortgage rates over the next several months. . . .”

What Does This Mean for You if You’re Looking To Buy a Home?

With both mortgage rates and home values expected to increase throughout the year, it would be better to buy sooner rather than later if you’re able. That’s because it’ll cost you more the longer you wait. But, there is a possible silver lining to buying a home right now. While you’ll be paying a higher price and a higher mortgage rate than you would have last year, rising prices do have a long-term benefit once you buy.

If you purchase a home today valued at $400,000 and put 10% down, you would be taking out a $360,000 mortgage. According to mortgagecalculator.net, at a 4.42% fixed mortgage rate, your mortgage payment would be $1,807 a month (this does not include insurance, taxes, and other fees because those vary by location).

Now, let’s put that mortgage payment into a new perspective based on the substantial growth in equity that comes with the escalation in home prices. Every quarter, Pulsenomics surveys a panel of over 100 economists, investment strategists, and housing market analysts about their expectations for future home prices in the United States. Last week, Pulsenomics released their latest Home Price Expectation Survey. The survey reveals that the average of the experts’ forecasts calls for a 9% increase in home values in 2022.

Based on those projections, a $400,000 house you buy today could be valued at $436,000 by this time next year. If you break that down, that means the equity in your home would increase by $3,000 a month over that period. That’s greater than the estimated monthly payment above. Granted, the increase in your net worth is tied to the home, but it is one way to put the home price appreciation to use in a way that benefits you.

Bottom Line

Paying a higher price for a home and a higher mortgage rate can be a difficult pill to swallow. However, waiting will just cost you more. If you’re ready, willing, and able to buy a home, now will be a better time than a year, or even six months from now. Let’s connect to begin the process today.